How I Turned My Art Training Costs into Tax Wins—Practical Lessons Learned

Paying for art training felt heavy on my wallet—until I realized I could ease the burden legally. Like many, I overlooked how education expenses could work for me at tax time. I tested deductions, documented every receipt, and learned what truly counts. It wasn’t about loopholes—it was about compliance done right. Now, I’m sharing what actually worked, so you don’t fall into the same traps I did. What started as a personal effort to reduce financial stress became a lesson in empowerment. Understanding how tax rules apply to creative learning transformed my approach to both budgeting and long-term planning. This isn’t a story about getting something for nothing. It’s about using the system fairly, responsibly, and effectively—so you keep more of what you’ve earned while investing in the skills you love.

The Hidden Cost of Creative Education

Art training carries a financial weight that often goes unmeasured. While the public may see only the final painting or sculpture, behind the scenes lies a steady stream of costs: tuition for workshops, fees for online courses, specialized software subscriptions, premium-grade materials, and even the time invested in practice and study. For many adult learners, especially those returning to education later in life or building skills outside formal degree programs, these expenses accumulate quickly. Unlike traditional students enrolled in accredited institutions, creative professionals and hobbyists pursuing skill development often assume they’re not eligible for financial relief. This assumption, widespread and understandable, leads many to absorb these costs silently, treating them as personal expenditures with no return. Yet this mindset overlooks a critical truth: education that enhances professional ability can qualify for tax benefits, even if it doesn’t lead to a degree.

The real cost of creative education isn’t just monetary—it’s also emotional and psychological. Paying out of pocket for training can feel like a luxury, especially when household budgets are tight. Many women in the 30–55 age range, balancing family responsibilities with personal goals, face this dilemma regularly. They may pause or abandon training due to cost, not lack of interest. But when viewed through a financial planning lens, these expenses take on new meaning. Each dollar spent on skill-building can be an investment, not just a deduction. The shift begins with recognizing that the IRS does not require a college degree path to qualify for education-related tax advantages. What matters is the purpose: is the training intended to maintain or improve skills used in a current trade or business? If so, it may be deductible. This principle opens the door for artists, crafters, designers, and other creatives to reclaim part of their investment.

Another overlooked factor is the cumulative impact of small, recurring expenses. A $30 monthly software subscription, $50 spent on canvas and paint, or $150 for a weekend workshop may seem insignificant in isolation. But over a year, these items can total thousands of dollars—money that, if properly documented, could support a legitimate deduction. The problem arises when these costs are not tracked consistently. Without a system, receipts get lost, memories fade, and opportunities vanish. The burden of creative education isn’t just in the spending; it’s in the missed chance to offset that spending through legal means. By reframing art training as a professional development activity rather than a personal indulgence, individuals can begin to see their expenses not as losses, but as strategic inputs with potential financial returns.

Why Tax Compliance Isn’t Just for Accountants

Tax compliance is often seen as a technical chore reserved for professionals, but in reality, it’s a form of personal financial protection. For creative learners, understanding and following tax rules isn’t about memorizing complex codes—it’s about making informed choices that safeguard both current savings and future stability. When education expenses are reported correctly, they become part of a broader strategy to reduce taxable income while staying within legal boundaries. This is not tax evasion, which involves concealing income or falsifying records; this is tax avoidance, a legal and responsible approach to minimizing what you owe by using available deductions and credits. The distinction is crucial. One carries risk and consequences; the other reflects diligence and awareness.

Many people avoid claiming education-related deductions because they fear drawing attention to their returns. They worry that filing certain forms or listing unusual expenses might trigger an audit. While audits are a possibility, they are not automatic—and they are far less likely when documentation is accurate and claims are reasonable. The real danger lies not in claiming legitimate deductions, but in failing to do so due to misunderstanding or fear. By choosing compliance, individuals protect themselves from errors that could lead to penalties or interest charges. At the same time, they position themselves to benefit from the full scope of what the tax system allows. This is especially important for self-employed artists or those building freelance careers, where every deduction can have a measurable impact on net income.

Compliance also builds confidence. When you know your records are complete and your claims are justified, you approach tax season with clarity rather than anxiety. This sense of control extends beyond taxes—it influences how you manage money throughout the year. You begin to think ahead, ask questions, and plan purchases with documentation in mind. For example, buying a new tablet for digital illustration becomes more than a creative decision; it becomes a potential business expense if used primarily for skill development or client work. The shift isn’t about changing behavior to fit tax rules, but about aligning natural goals—like learning and growth—with financial best practices. In this way, tax compliance becomes a tool for empowerment, not a burden. It turns passive spending into active financial management, giving individuals greater agency over their economic lives.

What Qualifies? Mapping Eligible Art Training Expenses

Not every expense related to art training qualifies for a tax deduction, but many do—provided they meet specific criteria. The key factor is purpose: the IRS generally allows deductions for education that maintains or improves skills needed in your current job or business, or that is required to keep your present position. This means that if you’re a graphic designer taking a course in advanced illustration software, those costs likely qualify. If you’re a stay-at-home parent learning pottery with no intention of selling work or teaching, the expenses probably don’t. The distinction hinges on professional relevance, not personal interest. This doesn’t mean you need to earn income from your art to claim a deduction, but there must be a clear connection between the training and your ability to perform or expand in a trade or business.

Qualified expenses typically include tuition for workshops, classes, or online courses offered by recognized instructors or platforms. These programs should have a structured curriculum and measurable outcomes, not just casual tutorials. Materials directly tied to the course—such as paint, brushes, clay, or specialized paper—may also be deductible if they are necessary for completing assignments or building skills. Software subscriptions, like those for digital drawing or photo editing, count when used primarily for professional development. Even travel costs can qualify under certain conditions: if you attend an intensive workshop in another city and the trip is primarily for training, not vacation, then transportation, lodging, and meals may be partially deductible. However, the burden of proof is on the taxpayer, so detailed records are essential.

There are clear boundaries. General supplies used for personal enjoyment, such as hobby-grade craft kits or decorative items, don’t qualify. Similarly, courses that are considered part of qualifying for a new trade or business—like someone with no prior experience taking a beginner class to start a craft business—may not be deductible in the early stages. The IRS draws a line between improving existing skills and acquiring new ones for a different career path. This means timing and context matter. Once the business is established, ongoing training to refine techniques or learn new tools becomes eligible. It’s also important to note that while degree programs at accredited institutions may offer additional tax credits, such as the Lifetime Learning Credit, these are separate from business expense deductions and have their own rules and income limits.

To determine eligibility, it helps to ask three questions: Is the training directly related to my current work? Does it enhance skills I already use professionally? Could I reasonably argue that this education helps me perform better in my field? If the answer to these is yes, the expense has a strong chance of qualifying. When in doubt, consulting a tax professional is wise. They can help assess whether a particular course or material meets the criteria based on your specific situation. The goal is not to stretch the rules, but to apply them correctly and consistently.

How I Structured My Deductions—Step by Step

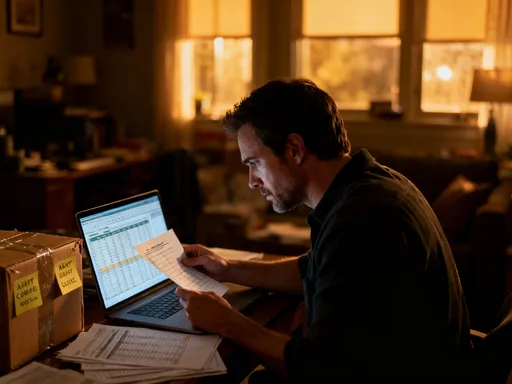

Turning theory into practice required a simple but disciplined system. I began by separating my art-related expenses from general household spending. This meant opening a dedicated folder—both physical and digital—where I stored every receipt, confirmation email, and invoice related to training. Each item was labeled with the date, purpose, and amount. For example, a $120 payment for an online watercolor course was filed with the course description and syllabus, showing it had a structured format and skill-building goals. Supplies purchased for specific projects tied to learning—like a set of professional-grade brushes—were also included, with notes on how they were used in class assignments.

Next, I categorized expenses into clear groups: tuition, supplies, software, and travel. This made it easier to match them with the appropriate sections of my tax return. Tuition payments were grouped by provider and course title. Supplies were totaled monthly and linked to the relevant training period. Software subscriptions, such as a $15-per-month illustration app, were tracked annually and prorated if used for both personal and professional purposes. For travel, I kept a log of dates, destinations, and the primary purpose of the trip. When I attended a five-day workshop in another state, I documented the schedule, confirmed the training hours, and separated personal sightseeing from official sessions. Only the portion of expenses tied to business use was claimed.

Timing was another critical factor. I aligned all expenses with the tax year in which they were incurred, not when the course ended. This meant recording a December payment for a January course in the previous year’s records. I also coordinated with my accountant early, sharing my organized files before filing began. This allowed us to review eligibility together and avoid last-minute surprises. Using tax preparation software helped ensure accuracy, as it guided me through the correct forms—primarily Schedule C for self-employed individuals or Form 2106 for unreimbursed employee expenses, depending on my income source. The process wasn’t about maximizing every possible dollar, but about claiming what was fair and defensible.

The result was a clean, auditable trail that supported my claims. I didn’t claim everything—I excluded items that were borderline or primarily personal. This approach gave me confidence when submitting my return. More importantly, it taught me to plan ahead. Now, I budget for training with taxes in mind, setting aside receipts from day one. What started as a reactive effort became a proactive habit, transforming how I manage my creative finances.

Balancing Risk and Reward in Education Tax Planning

Every financial decision involves a balance between opportunity and caution, and tax planning for education expenses is no exception. The reward is clear: reducing taxable income through legitimate deductions increases take-home funds and supports continued learning. But the risk—claiming too much, misrepresenting intent, or lacking proof—can lead to audits, penalties, or disallowed deductions. The goal is not to eliminate risk entirely, but to manage it wisely. This means focusing on substance over appearance, ensuring that every claimed expense reflects real, documented efforts to improve professional skills.

One of the most common pitfalls is inflating the professional relevance of a course or hobby. For example, taking a general painting class for personal enjoyment and labeling it as business training creates a mismatch between reality and reporting. The IRS looks for consistency: does your pattern of spending align with your stated profession? Do you have income from art-related activities? Are you building a portfolio, seeking clients, or teaching others? These factors strengthen the case for deductibility. Without them, isolated claims may appear arbitrary. It’s better to claim less with strong support than to claim more with weak justification.

Another risk involves mixing personal and business use. If a course has both recreational and professional elements, only the portion directly tied to skill development can be deducted. The same applies to supplies or software used for multiple purposes. A fair allocation method—such as tracking usage time or project types—helps maintain accuracy. Guesswork or arbitrary percentages raise red flags. Similarly, claiming expenses for family members, such as a spouse or child attending a class with you, is generally not allowed unless they are also part of your business. Overreaching, even with good intentions, undermines credibility.

The best defense against risk is transparency. Keeping detailed records, maintaining course materials, and preserving communication with instructors demonstrates intent and effort. If questioned, these documents tell a coherent story: you invested in training to grow professionally, and you did so honestly. This approach not only protects you but also reinforces responsible financial behavior. By prioritizing accuracy over maximization, you build a sustainable practice that supports long-term goals without inviting scrutiny.

Tools and Habits That Keep You Audit-Ready

Being audit-ready doesn’t require perfection—it requires consistency. The most effective tools aren’t complex or expensive; they’re simple systems that fit into daily life. I started with a digital folder structure on my computer, organized by year and category: “2023_Tuition,” “2023_Supplies,” “2023_Travel.” Each time I made a purchase, I saved the receipt as a PDF and filed it immediately. I also used a spreadsheet to log expenses, including date, vendor, amount, purpose, and course name. This allowed me to track totals in real time and spot patterns over the year. For recurring subscriptions, I set calendar reminders to update the log monthly, ensuring nothing slipped through the cracks.

Cloud storage added an extra layer of security. By backing up files to a trusted provider, I protected against loss from device failure or accidental deletion. I also enabled two-factor authentication to safeguard sensitive data. These habits took little time but provided significant peace of mind. Knowing my records were safe and accessible reduced stress during tax season. I no longer spent hours searching for scattered receipts or trying to reconstruct purchases from memory. Instead, I had a complete picture ready when needed.

Monthly check-ins became part of my routine. On the last weekend of each month, I reviewed recent transactions, confirmed they were logged, and adjusted categories if necessary. This prevented year-end overwhelm and made the annual tax process smoother. I also marked key dates on my calendar—tax filing deadlines, estimated payment due dates, and renewal dates for courses or software—so I could plan ahead. These small actions built a foundation of reliability.

The tools themselves are secondary to the mindset they support. Being organized isn’t about fear of audits—it’s about respect for your own financial journey. When you treat your creative development as a serious endeavor, you naturally want to protect and document it. These habits foster accountability, clarity, and confidence. Over time, they become second nature, turning compliance from a chore into a quiet advantage.

Turning Knowledge into Long-Term Financial Confidence

What began as an effort to reduce the cost of art training evolved into a deeper understanding of financial systems and personal agency. Learning how to claim deductions wasn’t just about saving money—it was about gaining control. Each documented expense, each reviewed receipt, each conversation with a tax professional added to a growing sense of competence. I stopped seeing taxes as an unavoidable burden and started viewing them as a framework within which smart choices could be made. This shift in perspective had ripple effects: I became more intentional about spending, more strategic about planning, and more confident in managing my finances overall.

Financial confidence isn’t built in a single year. It grows through repeated, responsible actions. By treating art training as a legitimate investment and aligning it with tax rules, I reinforced the value of my creative work. This mindset extends beyond deductions—it influences how I set goals, track progress, and measure success. I now see financial literacy not as a separate skill, but as an integral part of a sustainable creative life. When you understand how systems work, you stop fearing them and start using them to your advantage.

For other women navigating similar paths—balancing personal growth with practical responsibilities—this journey offers a powerful lesson. You don’t need to be an expert to benefit from the system. You just need to be informed, organized, and consistent. Start small: save one receipt, log one expense, ask one question. Over time, these actions build momentum. The goal isn’t to game the system, but to participate in it fully and fairly. When you do, you transform financial obligations into opportunities for empowerment. And in doing so, you create space—not just to survive, but to thrive—while doing what you love.